Tharisa: 48% Earnings Yield In A Tight PGMs Space.

1.8x PE Potential, 6% Dividend Yield, No Debt, Prime Assets, Potential to Double Production.

Summary

Platinum used to trade at a premium to gold, but have been dragged down by pessimistic demand forecasts that now seem too negative. Tharisa stands out in this environment: it owns Tier 1, low-cost mines and has managed to stay profitable despite depressed PGMs prices, unlike many of its peers. The company is in a net cash position, is family-led, trades at an earnings yield of 48% and offers a 6% dividend yield. If that’s not enough, it has the potential to double production.

Let’s discuss a few things first.

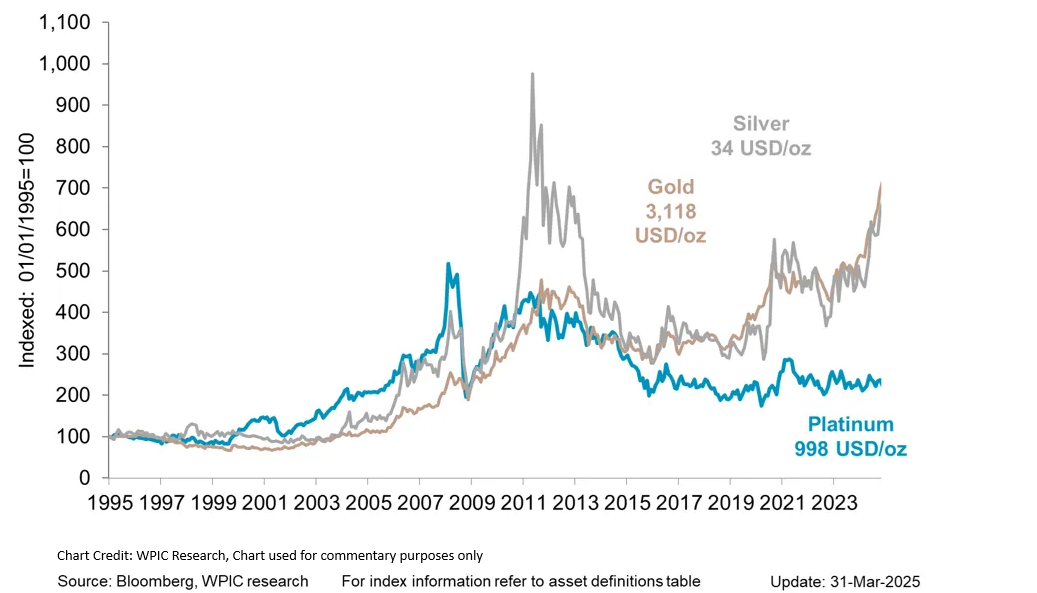

Platinum is an exceptionally rare and dense metal, about 20 times rarer than gold and 20% rarer than palladium. It’s also one of the heaviest metals, being 11% denser than gold and nearly twice as dense as silver. With a melting point almost twice that of silver, platinum possesses unique physical properties that set it apart in both industrial and investment applications. Because of this, platinum often traded at a premium to gold due to its rarity and industrial demand. From the early 20th century to around 2015, platinum was generally more expensive, with the platinum-to-gold ratio averaging about 1.2–1.5 meaning 1 ounce of platinum was worth 1.2–1.5 ounces of gold, as shown in this chart from WPIC:

In the last two years, gold has surged 66%, silver is up 31% but platinum has actually fallen 10%. That’s unusual, especially since these metals typically move in the same direction during uncertain times. What’s even more surprising is that platinum supply is expected to fall short of demand through at least 2029. So what’s going on with platinum, and more broadly, the platinum group metals (PGMs)? Could this gap be a chance to profit?

The prevailing narrative is that as battery electric vehicles (BEVs) gain market share, demand for PGMs will shrink. That’s because PGMs are mainly used in catalytic converters for internal combustion engines (ICE), and right now, there’s no clear alternative use big enough to make up for that lost demand. As a result, many expect these metals to face a long period of oversupply. Alright, now let’s look at some facts:

Battery electric vehicles have continued to grow, but their rollout has been slower than expected. Automotive use of the metal is now projected to decline by a much milder trend than previously feared:

“In the automotive sector, slowing demand growth in light vehicle electrification is entrenched. Accordingly, we expect a long tail in automotive platinum group metals (PGM) demand, with modest erosion of -1.4% CAGR for platinum and -1.0% CAGR for palladium through 2029f” - WPIC 06.02.2025

Hybrid and internal combustion engine vehicles have stayed much stronger than expected. In fact, some of the planned ICE bans in the US and EU are now being delayed or even reversed. Now, if I take a moment to grab a coffee and patiently fetch the data on new EU car registrations by power source over the past three years, here’s what the picture looks like:

It doesn’t look like Battery Electric Vehicles are on track to displace vehicles that use PGMs anytime soon. In fact, the share of PGM-using vehicles (hybrids and internal combustion engines) has only declined slightly, from 84.9% to 81.3% over the past three years in the EU. What we’re seeing instead is a clear shift in consumer preference toward hybrid vehicles, which actually gained the most market share. That resonates with me personally too, what would you choose as a consumer?

And yes, this data is from the EU, but the broader picture supports the same conclusion. In the US, consumer preferences still lean toward larger, heavier vehicles, which tend to favor PGM use. In developing markets, we’re not seeing a displacement of categories like in mature ones—car ownership is still expanding overall. That suggests volume growth across all segments, including those that rely on PGMs.

Beyond cars, platinum demand is holding up well. Jewellery and industrial uses—together making up a significant share—are expected to grow steadily at about 1% per year through 2029. While global jewellery demand peaked at 3 million ounces in 2014 and fell to 1.8 million in 2023, demand outside China has grown meaningfully: from 1.0 million ounces in 2014 to an estimated 1.6 million in 2024, helping to balance out China’s decline. In fact, even China is showing early signs of a fragile recovery, with modest growth expected next year, hinting that global jewellery demand may have already bottomed. Platinum is also benefiting from record gold prices, as some jewellers are swapping gold for the more affordable platinum to manage costs. Meanwhile, palladium’s sharp price drop is making it more attractive for industrial use. Source: WPIC.

What about the supply situation and the ongoing deficit?

Platinum market deficits, established in 2023 and 2024, are expected to persist through 2029. The World Platinum Investment Council projects average annual deficits of 672 koz from 2026–2029, equivalent to around 8% of demand. These are considered "largely structural" by WPIC CEO Trevor Raymond.

Above-ground inventories are tightening rapidly—down 23% to 3.38 million ounces in 2024, with a further 25% drop to 2.54 million ounces expected in 2025. Strategists from UBS suggest inventories may need to fall closer to 2 million ounces (so July 2026) before prices react more sharply to the undersupplied market.

On the supply side, global platinum production rose 3% to 7,293 koz in 2024 but is forecast to decline 4% to 7,002 koz in 2025. Recycling remains a drag, down 1% in 2024 to 1,486 koz—the lowest level in WPIC’s data series since 2013—and only a marginal recovery is expected in 2025 due to ongoing bottlenecks.

Overall I see an interesting metal, one that used to trade at a premium to gold, beaten down by pessimistic demand forecasts that are turning out to be too negative, while supply remains relatively weak.

PGMs had my curiosity, now they have my attention.

Tharisa PLC

To quickly get up to speed on the company and its assets, let’s take a brief step back:

Founded in 2008, with South African roots and a Cypriot base: Tharisa PLC was established by Loucas Pouroulis and incorporated in Cyprus. It’s listed on both the JSE and LSE, focusing on PGMs and chrome while drawing on Pouroulis’s deep mining background.

Tharisa Mine: a low-cost, open-pit producer since 2009: In operation since 2009, the Tharisa Mine has grown into a major mechanized, low-cost co-producer of PGMs and chrome.

Strategic growth in Karo Mining: Tharisa began investing in Karo Mining Holdings in 2018 with a 26.8% stake for USD 4.5 million, gradually increasing its ownership to 76.66% by January 2025, this is a Tier-1 PGM project.

As a result, Tharisa’s core focus lies in operating its flagship Tharisa Mine and advancing the Karo Project: its two main shows.

Located in South Africa’s Bushveld Complex, Tharisa Mine is an open-pit (for 11 years + option to go undergound) operation that produces both PGMs and chrome from the same ore body, something few mines do commercially. This reduces unit costs and places Tharisa in the lower cost quartile for both commodities in South Africa. This means that not only are the mining costs relatively low, but the dual revenue streams from chrome and PGMs also provide a natural hedge against fluctuations in commodity prices.

To put things in perspective, here’s how Tharisa stacks up against its peers, still not underwater despite the depressed PGMs prices:

Now, regarding the other main asset, Karo:

Tharisa holds a 76.22% stake in Karo Mining Holdings, with plans to raise it to 80%. Through this, it indirectly controls 85% of the Karo Platinum project, while the Zimbabwean government holds a 15% free-carry stake (i.e., no capital required). The government can acquire another 11%, potentially raising its stake to 26%.

The project sits on Zimbabwe’s Great Dyke, home to one of the largest PGM deposits outside South Africa, open pit and again low on the cost curve. With Special Economic Zone (SEZ) status, it benefits from tax breaks, duty-free imports, and currency flexibility, helpful offsets to today’s weak PGM prices.

So far, around USD 140 million has been spent out of an estimated USD 390 million. Given market softness, they’re sensibly progressing through smaller work packages tied to available funding, and commissioning has already been delayed. If prices remain low, further delays seem likely. Still, if brought online, Karo could more than double Tharisa’s output by adding 194,000 oz/year (6E basis), which would be lovely.

Overall, amazing assets. But before diving into how cheap the company is, we need to talk about management.

The Management

The chairman is Loucas Pouroulis, and the CEO is his son, Phoevos. Around 40% of Tharisa is owned by Medway Developments, whose beneficial owner is the Leto Settlement. In Tharisa’s filings we read this:

So here comes the other son, Adonis. This structure reflects significant family involvement in Tharisa’s ownership, which investors may evaluate when assessing governance and alignment with minority shareholders.

Public records provide additional context on the Pouroulis family’s broader business activities. A 2022 article by the Zimbabwe Independent noted that Kameni, a company associated with Loucas Pouroulis, was investigated by South African authorities for alleged false claims related to capital raising, though no wrongdoing was established, and Pouroulis denied the allegations [Zimbabwe Independent, 08.04.2022]. Separately, a 2019 article reported that 22% of shareholders at Petra Diamonds voted against the re-election of Adonis Pouroulis as a director [MiningM, 21.03.2019]. These events are not directly tied to Tharisa but they may be relevant for investors conducting comprehensive due diligence on management’s track record.

Moreover, Tharisa built its stake in Karo Mining Holdings partly by issuing shares to the Leto Settlement, which, being family-related, could raise considerations regarding potential conflicts of interest. That said, the amounts involved weren’t huge, so I won’t overreact.

Of course, there are merits here, again from a shareholder’s perspective. Loucas Pouroulis famously bought Impala Platinum’s Elandsfontein project for just $15 million and flipped it two years later to Xstrata for a staggering $1.1 billion. Clearly, the man knows how to spot value and secure quality assets, which lends credibility to both the Tharisa and Karo projects. On top of that, the Pouroulis family is wealthy, deeply rooted in South Africa, and likely very well-connected. That kind of network probably helps offset some of the operational risks that come with doing business in South Africa and Zimbabwe, and it’s arguably the most important point in our value equation.

Overall, I see this as the main risk when investing in Tharisa: will management truly act in the best interests of shareholders? The track record within Tharisa looks ok but given a few things in their broader history that I’m not personally entirely comfortable with, this is something I’ll be watching closely as a shareholder. Still, the above concerns aren’t significant enough for me to rule out the investment altogether so, ok, let’s go ahead and assess how cheap this company is.

My Value Ramblings

Let’s start with this: the company holds US$186.0 million in cash and carries US$106.7 million in debt, resulting in a net cash position of US$79.3 million. Adjusting the market capitalization for this, the enterprise value COMES DOWN to roughly US$140 million.

To put things in perspective, the company generated US$102 million in free cash flow in 2021. That’s a 72% return on EV in just one year (assuming similar PGMs prices), that's pretty impressive. The earnings yield, based on 2024 net profit from continuing operations and excluding other comprehensive income, is approximately 48% per annum, wow.

But before we get ahead of ourselves, let’s check some numbers:

As usual, I’d like to start with some very depressed assumptions. Let’s say US$1,500/oz for Iridium, US$4,400/oz for Rhodium, US$270/oz for Ruthenium, and US$800/oz for both Palladium and Platinum. Using the prill split provided in the Tharisa report, that translates to a basket price of approximately US$1,112/oz. For chrome, I’ve assumed a price of US$263 per tonne. These figures are significantly below recent market averages—and if you’ve been tracking PGM prices, you’ll see just how depressed this set of assumptions is. For example, Iridium is currently plateauing around US$4,000/oz and I’m considering just US$1,500/oz. Yet with annual production of 144,000 ounces of PGMs and 1.5 million tonnes of chrome, these inputs get us close to breakeven!

Now with more reasonable assumptions. Let’s say Iridium stays at US$4000, US$5000/oz for Rhodium, US$400/oz for Ruthenium, and for simplicity US$1000/oz for both Palladium and Platinum. This leads the average basket price to US$1446/oz, up 6% from the 2024 average price of US$1362. In this case, using 2024 chrome prices and volumes, net profit could be around US$90 for a P/E of 1.8 (earnings yield of 55%!).

Now, everything else being equal, if you believe Rhodium can reach US$25000/oz then the bottom line could spike to US$250 mio, almost double the EV!

And I’m not even considering Karo, which, if successful will double PGMs volumes.

All things considered, I think the pessimism around PGMs is a bit overdone and the 6% dividend yield makes the wait a little easier to swallow. Tharisa looks cheap enough to justify taking on some Zimbabwe and South Africa risk. That said, related parties transactions are a risk and if we do slip into a recession, PGMs and Chrome demand will take a hit.

Disclaimer: I own shares at the time of writing.

Sincerely,

The Boredom Baron

Disclaimer:

The content of this article reflects my personal views and is provided for informational and educational purposes only. It does not constitute investment advice, financial advice, or a recommendation to buy or sell any securities or financial instruments.

While I strive for accuracy, the information presented may contain errors or omissions, or be based on sources believed to be reliable but not independently verified. I make no representations or warranties as to the completeness, accuracy, or timeliness of any information presented.

This article is not intended to provide, and should not be relied upon for, investment, legal, tax, or accounting advice. The securities and strategies discussed may not be suitable for all investors. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

I may hold, or have held, positions in the securities mentioned. I do not receive compensation for writing this article, nor do I intend to influence the price or trading volume of any security discussed. All opinions are subject to change without notice.

This content is written strictly in a personal capacity and does not reflect the views of any employer, organization, or associated entity. Readers are strongly encouraged to conduct their own independent research and to consult with a licensed financial advisor before making any investment decisions.

Related Parties (and transactions) is a huge red flag to me. Probably need to dig through all their family history if they ever shafted shareholders.

Then there is the Karo mine which is a dud at these PGM prices. NPV at 10% and 11y is $68mn where 68% goes to Tharisa. And if you consider they already sunk 137mn its actually negative... bad capital allocation.

Great write up, thanks! I do have a question - I read the dividend has been cut by more than 50% last year. I am aware of the (cyclical) risk, but the 6% waiting reward…is not a sure thing it looks like. Did you check this cut / take it into account?