Boredom Baron — Weekly Intelligence Briefing (13 March 2026)

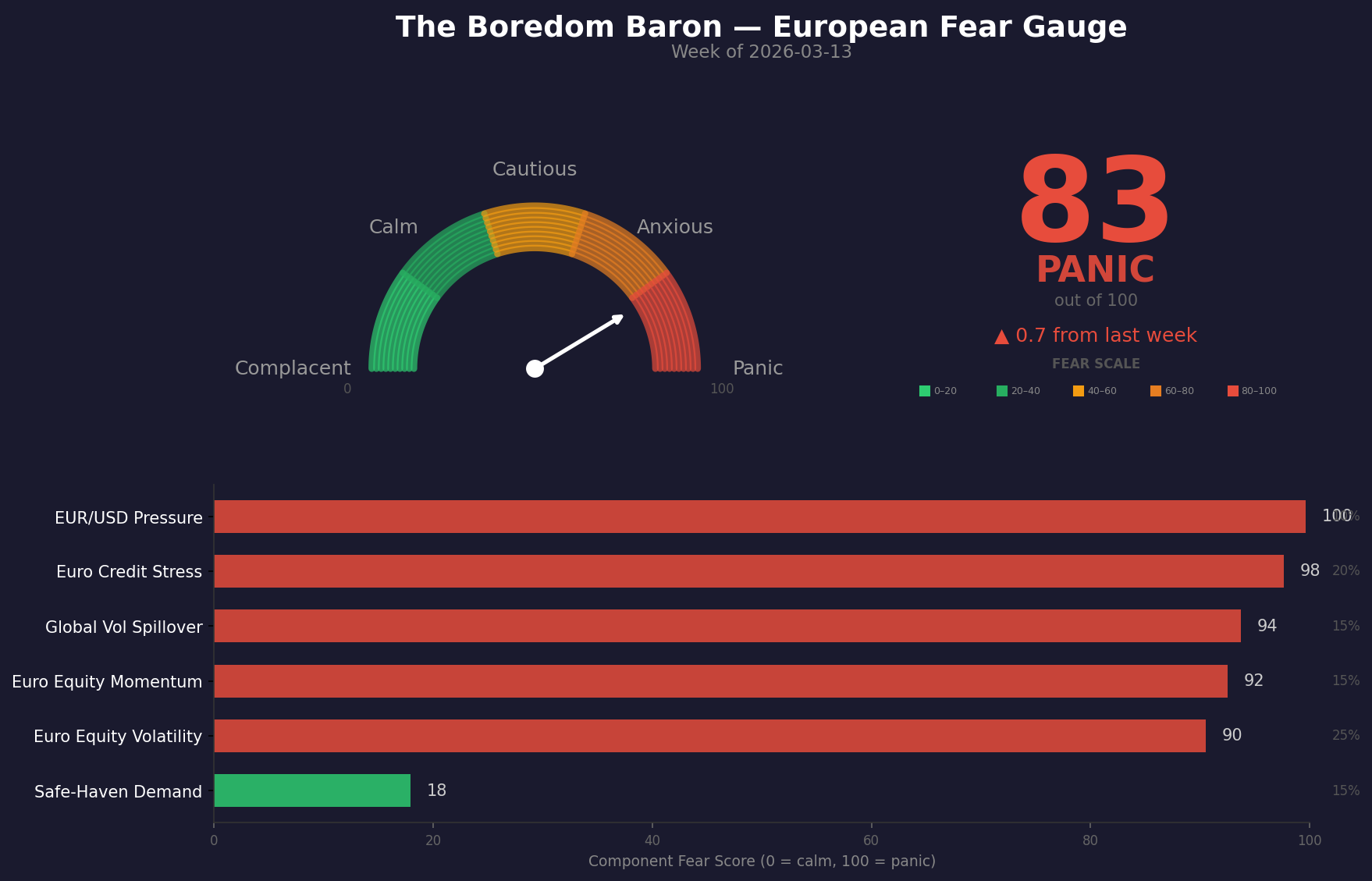

At a Glance: Fear Gauge 83/100 🔴 PANIC (prev. 82) | Sentiment -4.3 🟠 BEARISH (prev. -5.0)

You know what’s scarier than a Fear Gauge reading of 83? A Fear Gauge reading of 83 that barely moved.

Last week, I sat down with you and walked through the most violent single-week repricing this system has produced. The Fear Gauge leapt 38 points to 82. Every sentiment dimension was negative. I used phrases like “screaming” and “panic button,” and I hope I earned the right to use them by backing them up with data. This week, with oil closing above $100 for the first time since 2022, with Iran’s new supreme leader vowing to keep the Strait of Hormuz closed as a “tool of pressure,” with three more cargo ships struck in the Persian Gulf, and with the IEA calling this the largest disruption in history to oil supplies, the gauge ticked up 0.7 points to 83.

Zero point seven.

I want you to sit with that for a moment, because it tells you something profound about where markets are right now. Either last week’s repricing was so complete that the worst is already priced in, or markets have become numb to escalation. Both interpretations are plausible. Both have radically different implications for what you should do next. And figuring out which one is correct is, I think, the most important analytical question in European markets right now.

So let’s do what we always do. Let’s be good students. Let’s walk through the data, stress-test the narratives, and, because I know you’ve come to expect it, offer a few ways of looking at this crisis that you won’t find in any other briefing.

The Dog That Didn’t Bark

I’m going to start with what I think is the most underappreciated signal of the week, and it’s not oil at $100 or the Hormuz closure. It’s the composition of the Fear Gauge itself, specifically what changed and what didn’t.

Let me walk you through the components, because the devil really is in the details here.

EUR/USD Pressure went from 90 to 100. The euro declined roughly 3.1% against the dollar in a single week, a move that sits at the 0.4th percentile of historical weekly changes, meaning the velocity of this decline is more extreme than 99.6% of all observations in the dataset. To be clear, the euro at 1.15 is not a weak currency in absolute terms. What's alarming is how fast it moved. A 3% weekly move in a major currency pair is a disorderly repricing, not normal volatility. Last week, I told you the market was saying, "I want dollars, and only dollars." This week, the pace of capital exiting euro-denominated assets has intensified to near-record levels.

Euro Credit Stress went from 90 to 98. Near maximum. Last week, I flagged credit stress as the canary in the coal mine, the indicator to watch for a transition from a currency-driven panic to a credit-driven one. We’re not there yet, but we’re getting uncomfortably close. European high-yield is under severe pressure, and the FT’s reporting on “uncomfortable moments in private credit” suggests the liquidity picture in mid-market lending is deteriorating faster than public markets reflect. The Treasuries Fear Gauge, surging to nine-month highs, is confirming that this isn’t just a European phenomenon. Global fixed income is repricing risk.

Global Vol Spillover (VIX) went from 88 to 94. The VIX at 27.29 sits at the 94th percentile of historical readings, firmly in elevated territory, though worth noting this is nervous-market volatility, not March 2020 panic (when the VIX touched 82). The signal is loud, but it hasn't gone vertical.

Euro Equity Momentum went from 87 to 92. The selloff continues, but the acceleration is fading. The Euro Stoxx is down roughly 4.4% on a momentum basis, which is painful but not the kind of disorderly collapse that triggers forced liquidation cascades.

Euro Equity Volatility (VSTOXX) held at 90. Dead flat. Last week, this component's score surged by 71.7 points as the VSTOXX repriced sharply from complacency to anxiety. This week, nothing. The VSTOXX has settled around 22.7, which is elevated but not the kind of white-knuckle readings we saw during COVID or the early Ukraine shock. It's found a new, nervous equilibrium. That tells you the market has digested the initial shock and is now waiting for the next shoe to drop rather than actively panicking. Stabilisation at anxiety beats escalation toward chaos.

And then there’s the one that made me put down my coffee and stare at the screen for several minutes.

Safe-Haven Demand collapsed from 40 to 18.

Let me remind you of the trajectory here, because it’s extraordinary. Two weeks ago, Safe-Haven Demand was sitting at 3.6. Last week it surged to 40, an 11x jump that I described as “a violent signal that capital is actively seeking shelter.” I specifically noted that gold was declining despite a live shooting war, which I called an anomaly worth watching.

This week, gold is set for another weekly drop even as the Mideast war keeps oil prices high. Safe-Haven Demand didn’t just fail to keep surging. It crashed back toward the floor. A score of 18 means gold is actively falling in an environment where five of the six other fear components are above 90. In the history of financial markets, I struggle to think of a precedent where the traditional safe-haven bid evaporated during a genuine geopolitical crisis of this magnitude.

What does this mean? Let me offer three interpretations, ranked by how comfortable they make me feel (spoiler: none of them are comfortable).

Interpretation 1: This is the dollar, stupid. The simplest explanation is that the dollar’s rally is so powerful that it’s overwhelming every other signal. Gold is priced in dollars. When the dollar surges, gold falls in dollar terms even as real demand for physical gold rises. Under this reading, Safe-Haven Demand isn’t really falling; it’s being masked by FX effects. This is the most benign interpretation, and it’s probably partially true.

Interpretation 2: The market is pricing energy, not systemic risk. A more interesting explanation is that investors have decided this crisis is fundamentally about energy supply repricing, not about financial system integrity. In a classic systemic panic (2008, early 2020), gold surges because the question is “will the financial system survive?” In an energy supply shock, the question is “who gets the oil?” Gold doesn’t help you buy oil. Dollars do. If this reading is correct, it suggests the market thinks the banking system, payment rails, and sovereign credit structures are basically fine, even as energy markets convulse. That’s actually a constructive signal buried inside a terrifying headline number.

Interpretation 3: Margin calls are forcing gold liquidation. The least comfortable explanation is that institutional investors are selling gold to meet margin calls elsewhere in their portfolios. When equity volatility spikes and credit spreads blow out, leveraged investors need cash. They sell whatever is liquid. Gold is liquid. Under this reading, the decline in Safe-Haven Demand is a distress signal rather than a sentiment signal. I’m watching physical gold premiums (which would diverge from paper prices if this explanation is correct) to test this hypothesis.

I think the truth is a blend of all three, with Interpretation 2 doing most of the explanatory work. And if Interpretation 2 is correct, it has profound implications for the contrarian thesis I laid out last week, which I’ll return to below.

The Strait of Hormuz: From Closure to Selective Blockade

Last week, I described the Hormuz closure as the core problem driving the crisis. This week, the picture has become more nuanced, and in some ways more troubling, than a simple “the strait is closed.”

Here’s what actually happened. Iran’s new supreme leader, Mojtaba Khamenei, issued his first public message declaring that the strait will “remain closed” as a tool of pressure. Three more cargo ships were struck, with Iran warning of oil prices hitting $200 if the conflict continues. Oil tankers remain trapped in the Gulf as “sitting ducks” while Iran widens its attacks on shipping.

But here’s the detail that most briefings are glossing over, and it changes the analytical picture substantially: Iran is still shipping its own oil through the supposedly closed strait. CNBC reported this week that Iran has sent at least 11.7 million barrels of crude oil through the Strait of Hormuz since the war began, virtually all of it destined for China. The closure isn’t a closure. It’s a selective blockade. Iran controls who transits and who doesn’t, and it’s using that control to maintain its own export revenues while strangling competitors.

Think about what this means for the architecture of global energy markets. Last week, I described a tiered system emerging in which access to energy depends on bilateral political relationships with Washington (Germany gets a Rosneft exemption; India gets a Russian crude waiver). This week, we need to add a second axis to that framework: Iran is simultaneously running its own tiered system where access to Hormuz transit depends on your relationship with Tehran. China gets through. Everyone else doesn’t.

We are watching the real-time fracturing of global energy markets into competing spheres of influence, and I want to be explicit about why this matters more than the headline oil price for European small-cap investors. A world where oil is $100 but freely traded is uncomfortable. A world where oil is $100, and access depends on which political bloc you belong to, is structurally different. It means European companies cannot simply “hedge the oil price” and carry on. They need to assess which energy supply chains their governments have access to, which transit routes remain open to their flag states, and whether the political arrangements underpinning their energy security are stable. That’s a fundamentally different risk-management exercise from anything European industrials have faced since the 1970s.

Russia: The Shadow Winner Nobody Wants to Talk About

I’m going to say something uncomfortable, because I think it needs saying.

Russia is raking in an extra $150 million per day from surging oil prices. Let that number sink in. That’s roughly $1 billion per week in additional revenue flowing directly into Moscow’s war chest, revenue that funds the ongoing war in Ukraine, strengthens Russia’s geopolitical leverage, and insulates the Russian economy from Western sanctions that were supposed to be crippling it.

And the kicker? The US is now easing sanctions on Russian oil because energy prices have gotten too high. The very sanctions architecture that the West spent three years constructing to punish Russia for invading Ukraine is being dismantled to manage the consequences of a different conflict that the US itself initiated. (I am not making a political judgment here, but I am noting the irony, because it tells you something important about the constraints facing policymakers. When push comes to shove, energy security trumps geopolitical strategy. Every time.)

For European investors, this creates a deeply uncomfortable dynamic. Trump’s choices are pushing China and Russia closer together, precisely the geopolitical alignment that Western strategy has been trying to prevent for a decade. Russia benefits from high oil prices. China benefits from discounted Russian crude and continued Iranian oil flowing through its bilateral Hormuz arrangement. The losers are the countries (and companies) caught in the middle, which is to say, most of Europe.

Former European Council President Charles Michel said it plainly at the Global Baku Forum this week: what is happening today is “a gift for Russia” because oil prices are surging while attention shifts away from Ukraine. Azerbaijan is increasing gas deliveries to the EU to help fill the gap, but let’s be honest about the scale mismatch. Azerbaijani pipeline gas cannot replace 20% of global seaborne oil supply. It’s a sticking plaster on a severed artery.