The Unglamorous Bottleneck

How a four-billion-euro price tag on a maker of metal boxes tells you everything about the next decade of European grid spending

A Boredom Baron special report on European electrical grid equipment, June 2026. This is the free edition: the thesis, the three forces driving it, and a way to think about a sector that has gone from “what is a transformer” to “why is everyone suddenly shouting about transformers” in roughly eighteen months.

The members’ edition (dropping later this week) names the companies, scores the whole field, and builds a portfolio.

This is research and commentary, not investment advice, and certainly not a substitute for thinking.

1. A four-billion-euro price tag on a maker of metal boxes

The most revealing number in European industrials this month did not come from a company anyone has heard of. It came from SGB-SMIT, a transformer maker in Regensburg that ninety-nine percent of professional investors could not have identified in a police lineup three years ago, which is now reported to be testing the public market at a valuation north of four billion euros. Four billion. For a company whose entire reason to exist is to manufacture large metal boxes that make electricity a different voltage than it was a moment ago.

Read that again, because the instinct is to assume a typo. There is no typo. On a reported forward EBITDA of roughly 300 million euros, the talked-about price tags the business at around thirteen times earnings before all the things accountants like to add back. That is not a multiple the market hands out for making boxes. It is a multiple the market hands out for owning a chokepoint, and a transformer maker, it turns out, owns one of the best chokepoints in the industrial economy.

Here is the part the energy-transition brochures bury under photographs of wind turbines at golden hour. Transformer, switchgear and cable makers sit at the single narrowest point of three separate spending waves that have, with no coordination whatsoever, decided to arrive at the same time. The electrification of everything that currently burns fuel. The integration of wind and solar into grids that were designed by engineers who would have laughed you out of the room if you had described the modern energy system to them. And, the gatecrasher nobody invited, the bottomless electricity appetite of the data centers being built to run artificial intelligence. Each of those, on its own, would keep these factories busy for a decade. Together they imply a genuine, physical, years-long shortage of exactly the boring equipment these companies happen to make.

So the four-billion-euro question is not whether the demand is real. It plainly is. The question is the one the brochures never ask: is this a durable structural shortage you can own for years, or is it the precise moment a private-equity owner sprints for the exit while the public is still applauding? Both can be true at once, which is what makes this interesting. The free edition lays out the demand, the supply, the money and the catch. The members’ edition does the part that actually pays for itself: it names the businesses, scores them on how much of this theme they genuinely capture versus how much they merely gesture at in an investor deck, checks every valuation by hand, and builds a portfolio. Read this far and you will understand the sector. Read the second half and you will know what to do about it, which is a different and considerably more profitable thing.

2. Three supercycles, one set of factories

Start with the demand, because for once the demand is not the usual analyst fan-fiction. It is arithmetic.

Electrification. The slow tectonic story is that the world is swapping things that combust for things that draw current: cars, heating, steelmaking, rail, whole industrial processes. All of it lands on the grid. The International Energy Agency, an organization not given to excitable language, puts it about as bluntly as it ever does: for every dollar spent on renewable generation, only about sixty cents goes to the grids and storage needed to make any use of it, and in every scenario it models that ratio has to climb toward one-to-one through the 2040s. Translation: for fifteen years the world has been enthusiastically building power stations and quietly forgetting to build the wires to carry the power anywhere. That bill has now come due, and it does not take a credit card.

Renewables integration. A grid built around a few hundred large, obedient power stations is a fundamentally different animal from one built around millions of small, weather-dependent ones that generate hardest precisely when nobody needs it. Connecting North Sea wind to southern German factories, or Spanish sun to French industry, demands high-voltage transmission, undersea cable, converter stations and a great deal of switchgear. ENTSO-E, the club of European grid operators, has costed a project portfolio worth roughly 328 billion euros to 2040, rising toward 863 billion of total electricity infrastructure by 2050, and helpfully notes that every euro spent returns more than two in system savings, which is the sort of return profile that usually requires a financial crime to achieve. Meanwhile the queue of renewable projects waiting to plug into the European grid runs to roughly 1,700 gigawatts, and curtailment, the polite phrase for switching off perfectly good clean power because the wires cannot carry it, cost the system an estimated 8.9 billion euros in a single year. We are, in other words, building wind farms we then pay to switch off. The wires, not the windmills, are the binding constraint, and have been for some time.

Artificial intelligence. And then, right on cue, the accelerant nobody had in their model. European data-center electricity demand is set to rise sharply by 2030, with credible estimates running from the IEA’s roughly 70 to 115 terawatt-hours up to McKinsey’s punchier near-tripling toward 150 terawatt-hours, or something like five percent of the continent’s power, from a rounding error. The binding constraint, yet again, is not the generation. It is the grid. In the established hubs of Frankfurt, London, Amsterdam, Paris and Dublin, the wait for a connection now runs seven to ten years against a build cycle of eighteen to twenty-four months. Ireland’s data centers already inhaled twenty-two percent of the entire country’s metered electricity in 2024 and are heading toward thirty. Great Britain’s connection queue has bloated past 700 gigawatts, which is several times what the country could conceivably need, a queue so absurd the system operator had to invent new rules to clear out the speculative tickets. Every one of those connections, when it eventually happens, needs transformers, switchgear and cable. This is not a demand forecast. It is a waiting list, and waiting lists do not get talked out of existence on an earnings call.

The point that ties the three together, and the one most thematic ETFs miss entirely, is that they share one set of factories. The transformer line serving a utility upgrading a substation is the same line the offshore-wind developer and the hyperscaler are both queuing for. They are fighting over the same scarce output. That fight is what turns a worthy infrastructure story into something far more valuable to an investor: a pricing-power story.

3. Why the supply side cannot simply answer

In a textbook, this is where the story ends. Demand surges, prices rise, capacity floods in, returns get competed away, and the analysts who wrote “structural” in their notes quietly delete it. The reason this cycle refuses to follow the textbook, and the reason a box maker can fetch thirteen times EBITDA without anyone calling security, is that the supply side physically cannot respond on anything like the usual timetable.

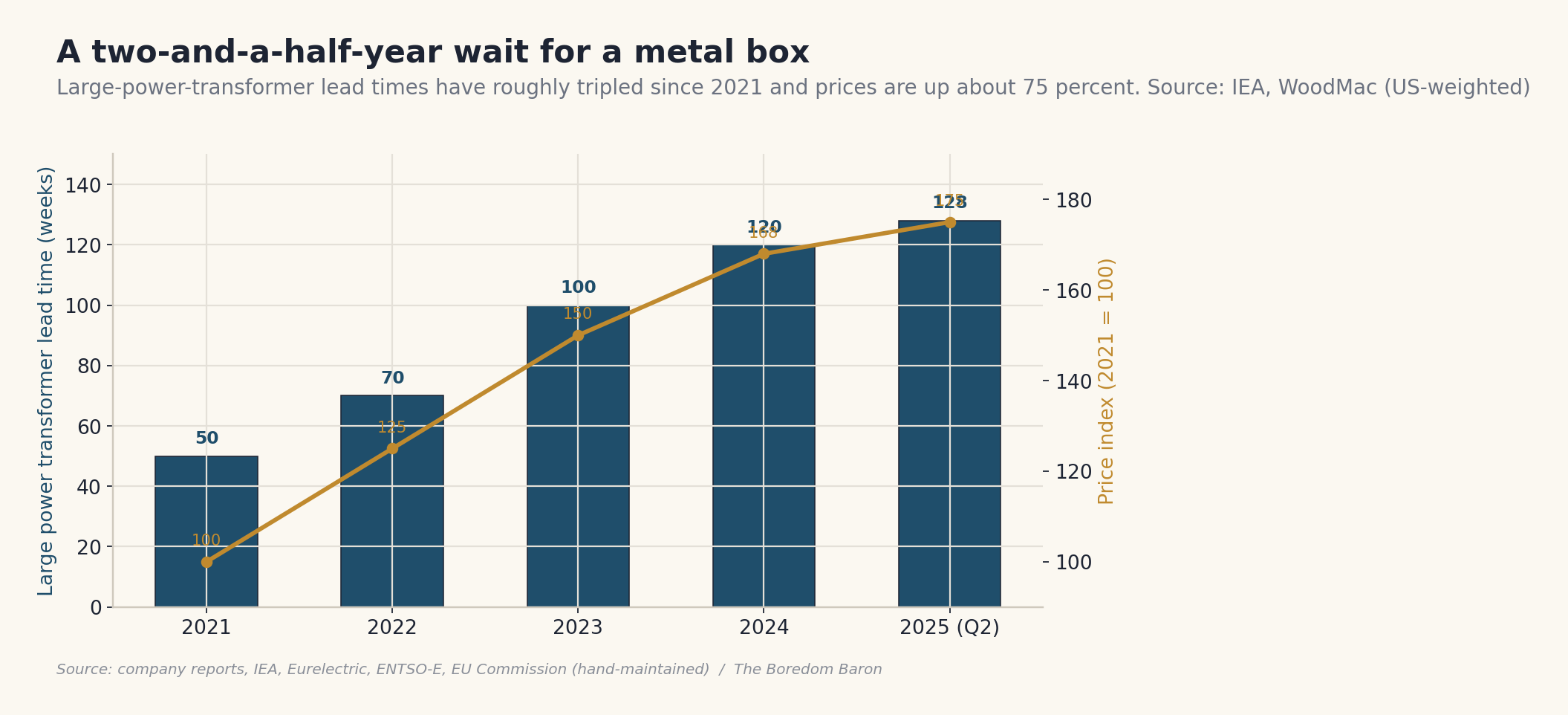

The wait for a large power transformer has gone from roughly fifty weeks in 2021 to about 120 to 128 weeks by 2025, with bespoke units quoted at up to four years, while prices have climbed on the order of seventy-five percent since 2019. When the customer is willing to wait the better part of three years and pay three-quarters more than they used to, you are not looking at a market about to be rescued by a wave of new supply. You are looking at a queue.

Three things keep the queue long. First, a critical ingredient, grain-oriented electrical steel, the specialized silicon steel transformer cores are wound from, comes from a handful of producers on earth and roughly doubled in price during the squeeze. You cannot conjure it. Second, the factories are slow and expensive to build and, more to the point, the people who know how to run them are genuinely scarce; the industry has announced well over twenty billion dollars of capacity expansion, but a new line takes three to five years to qualify and ramp, and a press release announcing a factory is not the same thing as a factory. Third, the genuinely hard end, the undersea cables and the high-voltage direct-current converters that link countries and bring offshore wind ashore, sits with three or four Western suppliers, and there is no express lane to becoming the fifth.

This is the entire difference between a trade and a cycle.

A bottleneck that clears in eighteen months is a trade, and you have probably already missed it.

A bottleneck that takes most of a decade to ease, against demand compounding the whole way, is a cycle, and cycles are where fortunes are actually made, usually by people patient enough to be bored.

The weight of the evidence says this one is the second kind. Which does not, and I cannot stress this enough, automatically make the shares worth buying.

See Section 7, where the good news goes to get expensive.

4. The money: how big, and how long it lasts

The scale of the spending behind this is the part that turns a nice story into a structural one, and it is large enough to be genuinely difficult to keep in your head.

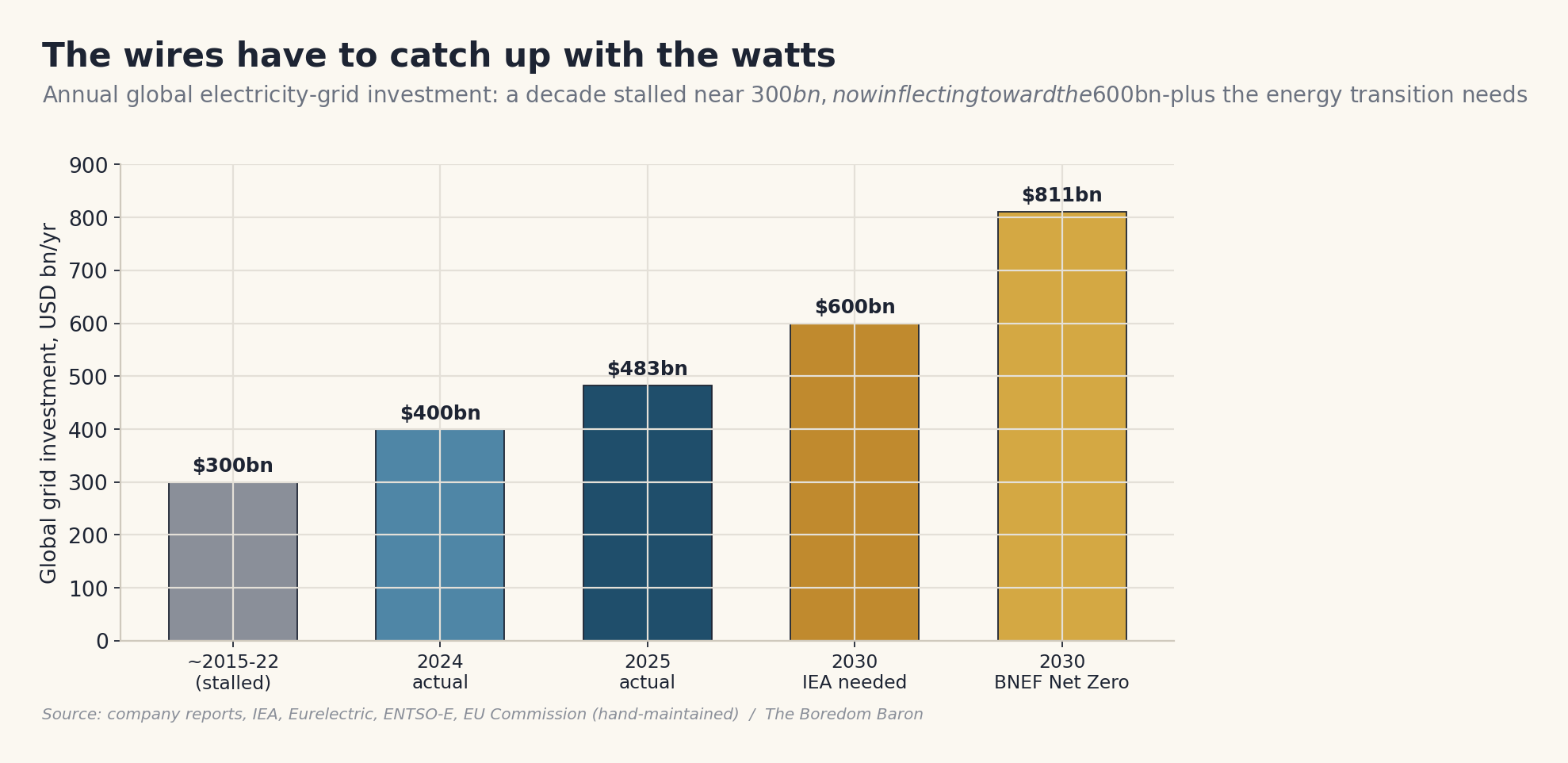

Global grid investment sat stuck near 300 billion dollars a year for over a decade, while generation spending nearly doubled around it, because building wind farms photographs better than burying cable and politicians have eyes. That neglect is now reversing in a hurry. The IEA reports roughly 400 billion dollars of grid spend in 2025, BloombergNEF counts it higher still, north of 470 billion and a record, and both agree it has to climb toward more than 600 billion a year by 2030 to keep the lights on and the targets credible. In Europe specifically, the Commission’s 2023 Grids Action Plan put the bill at 584 billion euros this decade, and by December 2025 it had stopped pretending that would be enough and sketched a modernization need of roughly 1.2 trillion euros through 2040. Roughly forty percent of the European Union’s distribution lines are over forty years old, which is a polite way of saying a good chunk of the continent’s electricity travels through equipment installed when the Berlin Wall was load-bearing. That is replacement spending, and replacement spending does not care about your views on the business cycle.

Now, a healthy skeptic will note that politicians announce trillions the way the rest of us announce diets, and that an EU communication is not a purchase order. Fair. So look instead at the people who actually take the orders, because order books do not lie the way press releases do. As of mid-2026, essentially every listed grid-equipment supplier is sitting on a record backlog. Hitachi Energy, the giant of the field, carries around 57.9 billion dollars of orders. Siemens Energy ended its half-year with a group backlog of roughly 154 billion euros, its grid arm growing orders more than forty percent. GE Vernova’s electrification orders are running at around two and a half times what it can actually ship. The cable specialists are sold out years ahead, locked in by frameworks such as TenneT’s roughly 30-billion-euro two-gigawatt program and National Grid’s 59 billion pound Great Grid Upgrade. When the whole industry’s book-to-bill sits comfortably above one, and above two at the sharp end, demand has stopped being the interesting question.

Execution has become it.

5. Where in the chain the scarcity actually lives

“Grid equipment” is not one business, and treating it as one is how investors overpay. It is a chain that runs from the heaviest, most specialized hardware at the top to the people who sell cable by the meter at the bottom, and the scarcity, the pricing power and the margin all pool at the top like cream. Where a company sits in this chain is the whole game, because two companies can both wave the word “electrification” at you while capturing wildly different amounts of the actual bottleneck, and only one of them deserves the multiple.

Node in the chainBottleneckMarginsWhat it actually isHVDC converters and high-voltage direct currentExtremeHighestThe kit that moves bulk power long distances and links countries; a three to four player clubLarge power and distribution transformersExtremeHighThe metal boxes; throttled by special steel and scarce laborHigh-voltage and subsea cablesExtremeBest-in-classThe wires for offshore wind and interconnectors; sold out for yearsHigh-voltage switchgear and gas-insulated gearHighHighThe protection and control that makes a substation more than a shedCable accessories and connectorsMedium-highHigh, asset-lightThe small parts a billion-euro project cannot finish withoutProtection, power electronics, componentsMediumHealthyFuses, surge protection, power-quality gear, busbarsGrid automation and digitalMediumHighest (software)The software that runs the networkGrid construction and installation (EPC)Medium-highThinThe people who actually dig the holes and stand up the steelElectrical distribution and wholesaleLowestThinnestThe merchants who stock it and sell it on

The single most useful idea in this entire report is that bottleneck severity and margin run in the same direction down that table, and that the companies the market most eagerly associates with “the grid” are frequently not the ones sitting highest on it. A diversified electrical giant may derive a surprisingly modest slice of revenue from the genuinely scarce top three rows, while an unfashionable mid-cap nobody covers may live almost entirely up there. Sorting the real bottleneck owners from the companies that merely sell into the general vicinity of a bottleneck is the work of the members’ edition. It is also, conveniently, where the cheap stock tends to be hiding.

6. The tell: when the insiders start selling

There is a second reason the SGB-SMIT story matters, and it is the one the bulls would rather skip. SGB-SMIT is owned by a private-equity firm that has held it since 2017, tried and failed to sell it outright in 2025, mused about parking it in a continuation fund, and is now reported to be testing the public market instead. Note the sequence. The professional buyers were offered this asset and passed; the plan to sell it to itself was floated; and only then did the public become the preferred customer. Nothing says “ground-floor opportunity” quite like being the third choice.

It is not alone at the exit. Pfisterer, a maker of high-voltage cable accessories, listed in Frankfurt in May 2025 and has since multiplied several times over from its offer price, which has every other private-equity owner in the sector reaching for a prospectus. A cluster of flotations and sponsor exits arriving simultaneously, while order books are at record highs and multiples are full, is one of the most reliable patterns in finance, and it does not signal early innings. It signals that the people who know these businesses best, the ones with the audited accounts and the customer contracts in front of them, have decided that the public market will pay them a richer price than a strategic buyer will. They are, in the politest possible terms, selling you the top of their own knowledge. This does not mean the cycle is over; the order books say it has years left to run. It means you should treat the supply of shiny new paper with the suspicion it has earned, insist on a price that makes sense, and decline to pay a scarcity premium to the very people offloading the scarce thing. The sellers know more than the buyers. They almost always do. That is why they are the sellers.

7. The catch: the boom is already in the price

Here is where the cheerleading note you may have read elsewhere and this one part company, and it is the reason this report exists in two halves rather than as a single excitable “buy the grid” sermon.

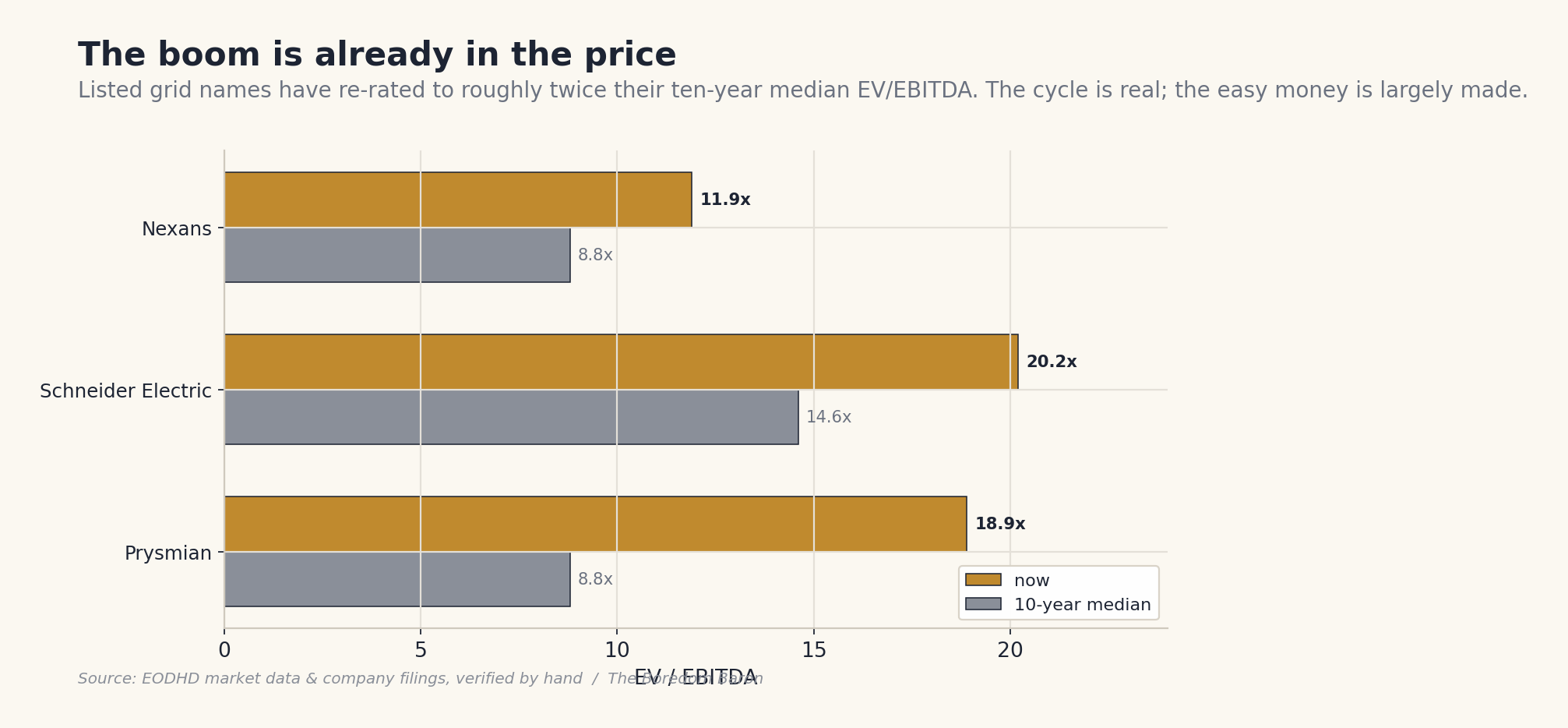

The market, irritatingly, is not asleep. The marquee listed grid names have re-rated to roughly twice their ten-year median valuations on enterprise value to EBITDA. The cable champion trades near nineteen times against a long-run median below nine. A leading electrical major trades around twenty against a median in the mid-teens. Many of these shares have doubled, tripled or worse over two to three years. The cycle is real, the demand is structural, and essentially all of that good news is now sitting in the price with its feet up. Buy the obvious names here and you are paying full freight for a cycle you are quietly assuming will run without a single stumble for the rest of the decade. The market has a long and entertaining history of punishing that assumption.

This is exactly where a value discipline stops being a personality trait and starts being an edge. There is a quiet, consistent and frankly underexploited pattern across this sector: the companies with the cleanest, purest exposure to the genuine bottleneck are disproportionately the smaller, duller, less-followed names trading on sensible multiples, while the companies wearing the richest valuations are often the big diversified ones whose true grid exposure is a minority of the business dressed up for the occasion. Theme purity and price, in other words, tend to pull in opposite directions. The crowd has bought the story. The bottleneck, at a fair price, is still sitting there largely unbothered in the part of the market that does not get written up in the weekend papers. Which names, and at what price each one stops being interesting and starts being a mistake, is precisely what the second half is for.

8. What could go wrong

No thesis this fashionable deserves to be read without its objections, and these are not garnish. They are the reason the members’ edition is selective rather than a shopping list.

The cycle is priced as though it is illegal for it to end. The largest risk is not that the demand fails to show up. It is that the demand shows up exactly as advertised, and shares already trading at twice their historical multiples deliver precisely what was promised and not one cent more. Re-rated cyclicals are merciless to companies that merely meet expectations.

This industry has blown itself up before, and recently. Electrical equipment has a well-documented habit of building too much capacity at the top. After the post-2008 stimulus, transformer capacity was thrown up with abandon and utilization in some markets collapsed within a few years. Today’s mid-to-high-teens margins sit comfortably above the through-cycle norm, and capacity is being added from three directions at once, by the incumbents, by a flood of Chinese exports, and by the Koreans. When supply finally catches demand, those peak margins are the first thing to mean-revert, and management teams currently describing the situation as a “supercycle” will rediscover the word “cyclical.”

The customers can simply stop. A great deal of this rests on rate-regulated utilities and on offshore-wind and data-center developers whose projects are exquisitely sensitive to interest rates, permitting and the political mood. Offshore-wind cancellations have already happened. A regulator squeezing allowed returns or a hyperscaler pausing to digest its own build-out would hit the order books that this entire thesis leans on.

The hard projects are genuinely hard. High-voltage direct-current and offshore work is fixed-price, first-of-its-kind and dependent on a dozen counterparties behaving. The sector’s own history is littered with large warranty and execution losses on exactly these contracts. One troubled mega-project can vaporize a year of a division’s profit, and the press release announcing it always uses the word “isolated.”

And a word on the data. A startling number of the headline figures in this sector mix transmission with distribution, different base years and different currencies, and a fair few of the rounder numbers come from press releases rather than anything audited. The members’ edition flags where the data is soft and corrects it where the public feeds are simply wrong, which, as we discovered, is more often than is comfortable.

The honest conclusion is that this is a genuine structural cycle wrapped in a partly delusional valuation. That combination is not an argument for avoiding the sector. It is an argument for being extremely particular about which slice of it you own and what you hand over for it, which is a value investor’s natural habitat and happens to be ours.

9. The one-paragraph version

Europe is about to spend more on its electricity grid than at any time in living memory, because three forces, the electrification of everything, the integration of renewables, and the gluttonous power demand of artificial intelligence, have arrived at once and all run through the same narrow set of factories that make transformers, switchgear and cable. The supply side cannot answer quickly, because lead times have tripled, a key steel is scarce, and the top end is a closed shop, so these companies have order books stretching years out and pricing power they have not enjoyed in a generation. The four billion euros being floated for one German transformer maker is the market pricing that bottleneck in public. The catch, and there is always a catch, is that the obvious names have already re-rated to roughly twice their historical multiples and the insiders are busy selling through new listings, which is the oldest late-cycle tell there is, so the easy money has been collected by people who are not you.

What remains is the part the crowd skipped: the cleanest exposure to the bottleneck sits in the smaller, cheaper, duller, less-followed names rather than the crowded large-caps, and exploiting that gap is the entire job description of a patient, valuation-disciplined investor.

Which is to say, it is our job.

10. What the members’ edition adds

This free edition hands you the map. The members’ edition hands you the territory, by name and with the receipts:

The whole field, scored. Two dozen listed European names across the entire value chain, each rated on how much of the theme it genuinely captures, the quality of the business, and the value actually on offer today, in one ranked table that will annoy anyone who owns the sector through the biggest name they could find.

Deep dossiers on the names that matter. Verified financials (every market cap and multiple recomputed by hand, because the public feeds are wrong on several, including one where the headline price was overstated by a fifth), order backlogs, ownership, the bull case and the bear case, and a blunt valuation verdict for each.

The cheap-and-clean opportunities, including the two names we think offer the best risk and reward in the entire sector, both of which you can buy today without holding your nose.

The names to avoid, including the one celebrated large-cap we think is priced for a perfection it has no chance of sustaining, and the statistically “cheap” names that are cheap for reasons that have precisely nothing to do with the grid.

A suggested portfolio, seven names with position sizes, the job each one does, explicit entry discipline on the ones to buy only when the market does you a favor, and a clear list of what would break the whole thesis.

Founding members get it first. It is the difference between knowing the grid is the trade and knowing how to own it without overpaying for the privilege.

Not investment advice. Do your own work. The boring possibility is, as I keep telling you, the under-priced one.

Sincerely,

The Boredom Baron

This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.

Disclaimer:

The content of this article reflects my personal views and is provided for informational and educational purposes only. It does not constitute investment advice, financial advice, or a recommendation to buy or sell any securities or financial instruments.

While I strive for accuracy, the information presented may contain errors or omissions, or be based on sources believed to be reliable but not independently verified. I make no representations or warranties as to the completeness, accuracy, or timeliness of any information presented.

This article is not intended to provide, and should not be relied upon for, investment, legal, tax, or accounting advice. The securities and strategies discussed may not be suitable for all investors. Past performance is not indicative of future results. All investments involve risk, including the potential loss of principal.

I may hold, or have held, positions in the securities mentioned. I do not receive compensation for writing this article, nor do I intend to influence the price or trading volume of any security discussed. All opinions are subject to change without notice.

This content is written strictly in a personal capacity and does not reflect the views of any employer, organization, or associated entity. Readers are strongly encouraged to conduct their own independent research and to consult with a licensed financial advisor before making any investment decisions.

This Substack is reader-supported. To receive new posts and support my work, consider becoming a free or paid subscriber.