Uncovering Opportunities Beyond MP Materials: The Rare Earths Race

From national security risks to investment opportunities: a detailed look at rare earth supply chains and key players.

Introduction

As discussed in previous posts, America’s virtually non-existent rare earth and permanent magnet supply chains have become a top national security concern. Since those articles, that urgency has started to show up in the markets with MP Materials surging over 100 percent in just a few weeks following major deal announcements.

This is the third article in my minerals series exploring investment opportunities. The first piece made the case for a commodity supercycle and shared four related stock picks. The second focused on the rare earths thesis, outlining why it matters, why it presents an opportunity and offering an overview of the main players in the space.

Today, we dig deeper. I will cover one well-known company, MP Materials of course, and introduce three under-the-radar names that are barely being discussed online.

Depending on how this piece is received (I will check the likes on the post!), I plan to close out the rare earths segment with one final article featuring Lynas and three more overlooked opportunities in the REE space. Otherwise, this critical minerals series will continue with other critical minerals also including silver and gold. And of course, this is just one series. Coverage of non-mining companies will continue as usual. So let me know:

What are we talking about?

Before diving in like a cannon into the rare earths companies, we need to lay out a some more few key aspects of the industry. I couldn’t find a solid article that compares most of the players in the rare earths space and none that take the time to explain the dynamics and distinctions that actually help you understand these companies without taking anything for granted for less experienced readers. You know what they say: if it doesn’t exist, do it yourself. So, let’s start there.

The below slide from MP Materials quickly explain how it works. First, rare earth ore is mined and crushed, then processed to concentrate the valuable minerals. Next, this concentrate is heated and treated with chemicals to separate out pure rare earth oxides. Finally, those oxides can be turned into metals and made into magnets.

After Stage 1, China holds a near monopoly, and that is exactly where the investment thesis starts to take shape. Most short reports miss the point. These are strategic assets, and when it comes to rare earths security of supply will take priority over cost, as I explained in previous articles even before the Apple and Pentagon deals were announced [linked here and here].

After my second article, one subscriber left a particularly well-received comment:

“[…] So the entire thesis here is contingent on a massive global conflict involving the U.S. and China, which is pretty hard to forecast.”

I’m not sure that’s the right angle. In my humble view, the real issue is that the West has finally recognized its deep dependence on China and that China is now willing to use that dependence as leverage. In response, the West will use this moment as a catalyst to aggressively diversify supply chains and reduce China’s leverage, regardless of whether a conflict materializes.

“First, the vulnerability is clear and so is the solution. For any nation outside China, the most urgent step toward securing a self-sufficient critical mineral supply chain is to invest in refining capacity. That’s why the global buildout of rare-earth oxide processing plants is already underway and poised to grow exponentially.”

This is already starting to take shape with the Department of Defense’s agreement to support a price floor of 110 dollars per kilogram for NdPr in its deal with MP Materials. As the chart below shows this is well above prevailing market levels and it sends a strong signal. By effectively covering part of MP’s pricing risk, the U.S. government is making it clear that securing supply matters more than short-term cost efficiency:

By 2030, rare earth processing capacity is expected to grow eightfold in the U.S. and Europe, triple in Africa, and rise by a factor of 29 in Australia, according to Benchmark Minerals Intelligence. These are just forecasts, of course, but as we’ve seen they make sense:

Two different stories

Now, let’s clarify some key differences among the rare earth elements, since understanding these will be crucial for our discussion of the companies below. To keep it simple let’s group the REEs as follows:

NdPr is the most commercially and strategically important rare earth product today. Over 90% of electric vehicle motors and a large share of wind turbines rely on NdPr-based magnets. No alternative material matches their performance in many critical applications.

For the heavy rare earths, I won’t bore you with the technicalities of ionic clays, the main point is that dysprosium (Dy), terbium (Tb), and yttrium (Y) are much harder to source. But that’s not all. Even when available, separating heavy rare earths like Dy and Tb is technically demanding, requiring over a thousand solvent-extraction steps and specialized expertise, almost all of which is based in China. Although used in small amounts, they are essential. These elements boost coercivity enough for magnets to perform reliably at 150 to 200 degrees Celsius, which is critical for EV traction motors, offshore wind turbines, and jet engine starters. Dy and Tb make up less than 5 percent of global rare earth production by volume but account for roughly 40 percent of the total market value because of their scarcity, complex processing, and crucial role in high-performance applications. So, if they’re missing, can you make EV motors or other applications without sacrificing significant performance? No, not for now.

Interestingly, the market for heavy rare earth elements is quite tight, and studies highlight an emerging shortage of both dysprosium and terbium. In addition, Academic research (using circumstantial evidence) support a theory that China has been drawing down its strategic stockpiles to mask underlying supply deficits. Although the exact size of these stockpiles remains classified, several indicators suggest systematic inventory depletion.

Given this context, having access to heavy rare earths and the capability to process them would be a national treasure in the West. This kind of strategic advantage is exactly what makes a company especially desirable.

We’re good to go now:

MP Materials

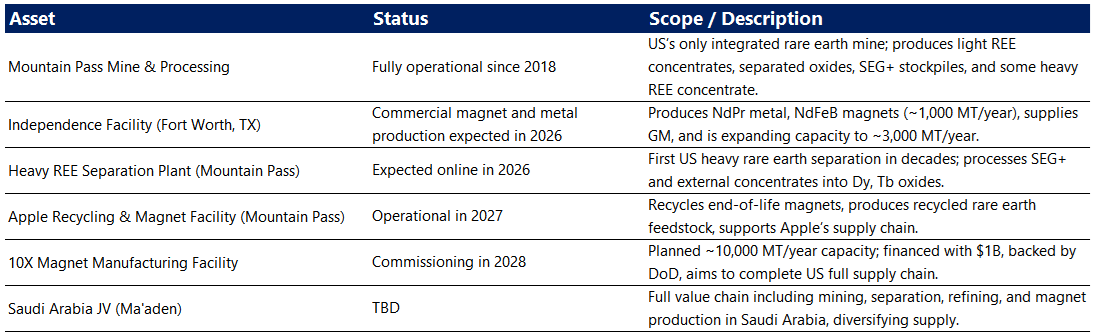

MP Materials' story begins with the acquisition of the Mountain Pass mine in 2017, when a consortium led by James Litinsky's JHL Capital Group purchased the dormant assets for $20.5 million out of bankruptcy. The Mountain Pass facility, originally discovered in 1949, had previously been the world's primary source of rare earth elements before Chinese competition forced its closure in 2015.

This is how we can summarize what they’re up to:

The Mountain Pass mine is one of the world’s highest quality rare earth deposits, with grades of 8 to 12 percent rare earth oxides, significantly higher than most global competitors. It is also the only fully integrated rare earth mining and processing facility in the United States. That is the story most headlines highlight. But dig a little deeper, and you will see that the ore body is rich in light rare earths like neodymium, praseodymium, lanthanum, and cerium, while containing very little dysprosium or terbium. And it does not stop there: they also do not refine heavy rare earths. That is why owning the company is not a no-brainer. The commercial oxide output is almost entirely composed of light rare earths. These are important but if you are not just making magnets for kitchen appliances and want to produce high-performance magnets, you will need dysprosium and terbium.

Until 2023 the United States had no commercial-scale separation plant, so MP Materials shipped Mountain Pass concentrate to China for refining. That pipeline shut down in April 2025 when Beijing retaliated against new U.S. tariffs by slapping a 125 percent duty on the material. Rather than sell at a loss, MP halted exports and began stockpiling concentrate (SEG⁺) while fast-tracking two domestic projects: (1) the expansion of its California refinery, which already upgrades roughly half of the mine’s output and will add a heavy-rare-earth circuit in 2026 to produce dysprosium and terbium oxides, and (2) the ramp-up of its Fort Worth, Texas, facility that turns separated oxides into metal and NdFeB magnets.

MP’s new magnet manufacturing facility in Fort Worth has begun small-scale production and is expected to start delivering magnets and alloys later this year under a long-term offtake agreement with General Motors. Notably, the plant has significant excess capacity beyond GM’s immediate needs, and MP is actively receiving interest from additional prospective customers. On the light rare earth front, MP has also optimized its downstream processing to quickly ramp up refined REO output (refined oxide form of rare earth elements after processing) when market conditions warrant. A $100 million prepayment from GM is helping fund this effort.

As those upgrades come online, the company will be able to process the SEG⁺ (it’s medium- and heavy-rare-earth concentrate) now piling up on site and convert it into finished magnets entirely within the United States.

To support the transition, the Department of Defense has acquired roughly a 15 percent stake in MP Materials and is providing a 150 million dollar loan on highly favorable terms to accelerate the development of its heavy rare earth separation capabilities. This is a major positive, as it gives the company a crucial cushion to move forward with heavy rare earth processing without being too exposed to weaker market conditions in the meantime.

What’s not interesting?

Overall, the Department of Defense partnership is clearly a positive for shareholders. It provides real downside protection through price floors and guaranteed demand. But let’s not ignore the tradeoff: this deal also caps upside through profit-sharing arrangements and limits flexibility.

MP Materials is projecting NdPr production of around 4,900 to 5,200 metric tons by 2028, with a target run-rate EBITDA of 650 million dollars. Full ramp-up is expected between 2027 and 2028. On paper, that sounds solid but delays have already happened for stage 2. So is it really a great deal to pay around 9 billion dollars today for such an EBITDA two to three years out? Maybe, if there were more room to run. But the upside here looks somewhat structurally limited.

More importantly, the company still doesn’t have a solution for heavy rare earth feedstock. Yes, they plan to separate heavy rare earths at Mountain Pass, but the geology just isn’t there. The mine barely contains any dysprosium or terbium. So even if they finish building the separation facilities, they’ll still have to source third-party concentrate from somewhere else.

“Mr Baron, but MP Materials is building separation facilities to process their own SEG+ concentrate, so geological limitations aren’t that important” you might say.

Sure, they do collect the remaining heavy rare earth fraction as SEG+ concentrate after separating the light rare earths. But that only adds up to about 50 to 60 metric tons a year, which is tiny compared to global (or US) heavy rare earth demand. They’ll still need third-party concentrate if they want to scale up in a meaningful way.

Here’s where it gets interesting. MP’s planned capacity will exceed what Mountain Pass alone can supply, so they’re designing their flow sheet to accept third-party feedstock.

Which makes you wonder: where is that feedstock supposed to come from? Because it’s definitely not coming from Mountain Pass. China again? Are there other players in the U.S. that could benefit from government backing? Can we find something better than MP?

Several U.S. and other Western projects are either producing or close to producing mixed or heavy rare earth concentrates. These could serve as important feedstock for MP’s separation plant when it becomes operational in 2026.

That opens up a different angle: maybe there’s better value in the small-cap developers. Let’s dive into those who aren’t making headlines but still have solid projects and credible backing. Since coverage is scarce or nonexistent, I listed their names in the last article but the deeper analysis should go behind the paywall to keep it limited.